Executive Summary: Key Technical Insights

- EU MRV Scope Expansion: Effective January 1, 2025, the EU Monitoring, Reporting, and Verification (MRV) system has expanded to cover all general cargo and offshore support vessels (OSVs) between 400 and 5,000 GT, bringing smaller commercial fleets into the regulatory net.

- EU ETS Integration: While large commercial vessels are already subject to the EU ETS, offshore vessels above 5,000 GT will enter the scope for surrender obligations starting January 1, 2027. Smaller OSVs (under 5,000 GT) remain exempt from purchasing allowances but are under active regulatory review.

- FuelEU Maritime Focus: Effective January 2025, FuelEU Maritime mandates a phased reduction in the greenhouse gas (GHG) intensity of energy used on board ships above 5,000 GT, pushing operators toward biofuel and alternative fuel pathways.

- Dutch Green Deal Targets: The Netherlands’ local *Green Deal Zeevaart, Binnenvaart en Havens* sets aggressive local targets, aiming for a 40–50% reduction in CO2 emissions from inland shipping by 2030 and at least 150 zero-emission inland vessels.

- ECA and National Policy Alignment: Synergies between EU-wide mandates, local Green Deals, and Sulphur/Nitrogen Emission Control Areas (SECAs/NECAs) are creating a unified framework driving zero-emission fleet deployment across the Baltic and North Seas.

Introduction

The global maritime industry is navigating its most significant regulatory transition since the shift from coal to oil. Europe is leading this change, utilizing a combination of carbon pricing, emissions monitoring, and fuel intensity limits to force a shift toward sustainability. These regulations are designed to align the maritime sector with the European Green Deal's goal of achieving a 55% reduction in greenhouse gas emissions by 2030 compared to 1990 levels, and full climate neutrality by 2050.

For workboat operators and fleet managers, these rules are no longer abstract policy concepts. With the implementation of key regulations in 2025 and 2027, the operational economics of commercial vessels in European waters are changing rapidly. Understanding these frameworks is essential not only for compliance, but also for protecting asset values and identifying cross-border opportunities. Fleet decisions made today will dictate the charter eligibility and resale potential of vessels for the next decade.

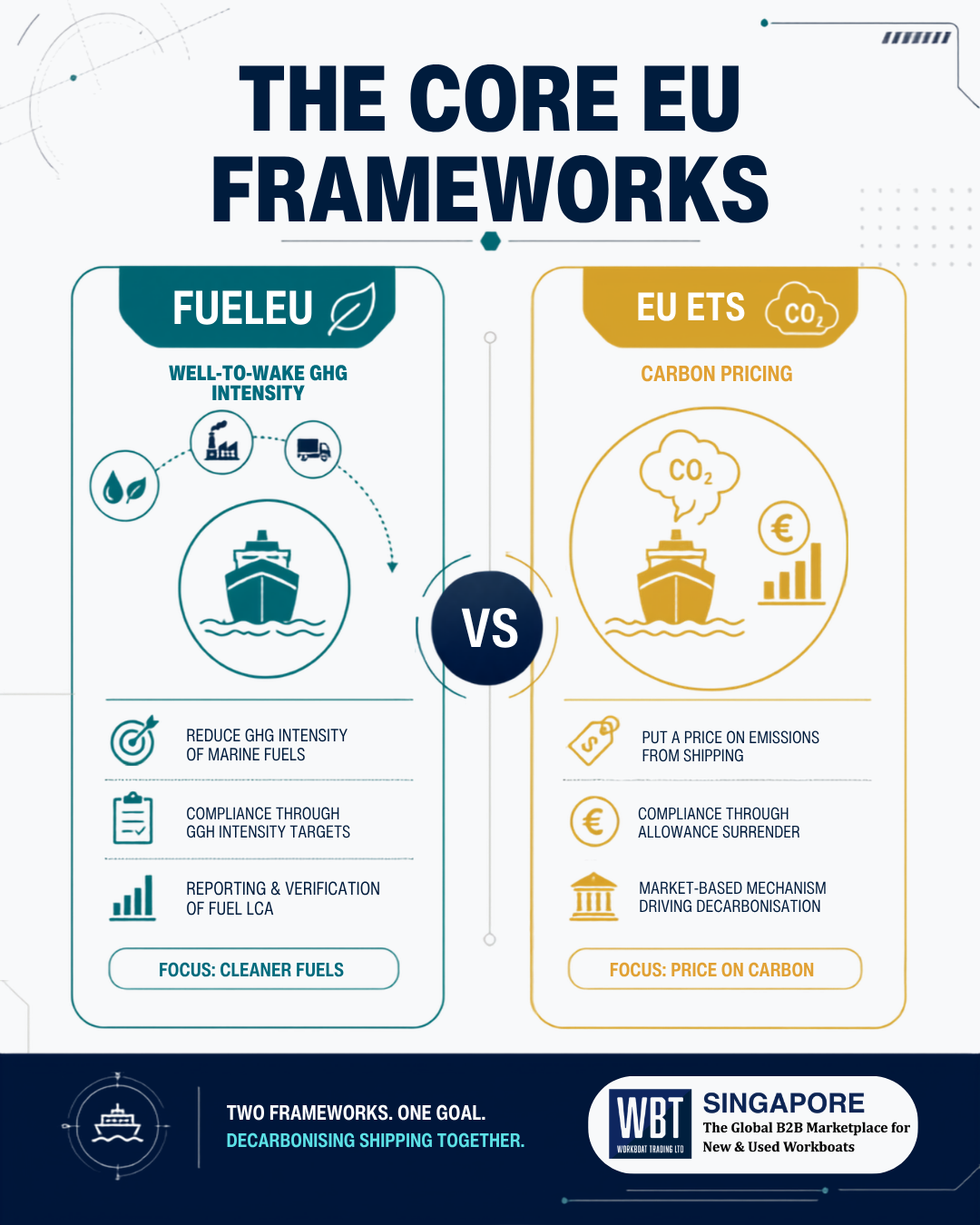

Deciphering the Core EU Frameworks: FuelEU Maritime vs. EU ETS

Two primary pillars drive the EU's maritime decarbonisation strategy: FuelEU Maritime and the EU Emissions Trading System (EU ETS).

FuelEU Maritime: Limiting Energy GHG Intensity

Effective January 2025, FuelEU Maritime focuses on the greenhouse gas intensity of the fuel consumed on board.

- The Target: The regulation mandates a phased reduction in the average GHG intensity (covering CO2, CH4, and N2O) of energy used on board, starting with a 2% reduction in 2025, scaling to 6% in 2030, and rising to 80% by 2050 compared to a 2020 baseline of 91.16 gCO2eq/MJ ($gCO_2eq$ of emissions per megajoule of fuel energy).

- Well-to-Wake Lifecycle: Unlike regulations that only monitor tailpipe emissions, FuelEU Maritime calculates emissions on a "well-to-wake" basis, accounting for the environmental impact of fuel production, transport, and distribution. Fuel emission factors are strictly calculated: standard Marine Gas Oil (MGO) is rated at approximately 94 $gCO_2eq/MJ$, whereas bio-methanol can be rated as low as 10–20 $gCO_2eq/MJ$ depending on the biomass source. Methane slip from LNG engines is heavily penalized, adding a methane factor ($CH_4$ factor) that can significantly inflate the vessel's calculated emissions index if the engine technology lacks high combustion efficiency.

- Penalties and Banking: If a vessel fails to meet the compliance target, the operator faces significant financial penalties—calculated at €2,400 per tonne of VLSFO (Very Low Sulphur Fuel Oil) equivalent deficit. However, the regulation allows for compliance banking (carrying forward a surplus) and pooling (averaging the compliance balance across a group of vessels), which offers commercial flexibility for fleet managers. If a fleet contains highly compliant zero-emission vessels (e.g., all-electric ferries), their surplus compliance balance can be pooled with diesel-powered support vessels to offset penalties across the company.

EU ETS: Pricing Carbon in European Waters

The EU ETS is a cap-and-trade system that puts a direct price on carbon emissions.

- Allowance Surrender Schedule: Shipping companies must purchase and surrender EU Allowances (EUAs) to cover their verified carbon emissions. The system has a phased implementation: operators surrender 40% of verified emissions for 2024, 70% for 2025, and 100% from 2026 onwards. EUAs are traded on the ICE exchange, and prices fluctuate based on market demand.

- Offshore Vessels: Offshore support vessels (OSVs) above 5,000 GT will enter the scope of the EU ETS for surrender obligations starting 1 January 2027. This means operators will have to pay for every ton of CO2 emitted during voyages between EU ports, and 50% of emissions for voyages entering or leaving the EU. Given that EUA prices frequently fluctuate between €60 and €100 per tonne of CO2, carbon pricing will directly impact daily charter rates. For example, an OSV consuming 10 tonnes of MGO per day emits approximately 31.8 tonnes of CO2. At an EUA price of €80 per tonne, this translates to €2,544 in compliance costs per operating day, which must be built into the charter rate.

- Vessels 400 – 5,000 GT: Smaller workboats in this range are currently exempt from purchasing allowances. However, they are subject to reporting requirements that lay the groundwork for potential future financial obligations.

The Direct Hit: EU MRV Expansion for Smaller Fleet Elements

The most critical immediate change for workboat operators is the expansion of the EU Monitoring, Reporting, and Verification (MRV) regulation.

Since 1 January 2025, the EU MRV system has applied to:

- Offshore Support Vessels (OSVs) between 400 and 5,000 GT.

- General Cargo Ships between 400 and 5,000 GT.

This means operators of tugboats, larger crew transfer vessels, utility barges, and medium-sized supply boats must actively log and report fuel consumption, distance traveled, and time spent at sea.

Permitted Monitoring Methods

Under the EU MRV, operators must choose from four permitted monitoring methods:

- Method A (Bunker Delivery Notes): Calculating fuel consumption based on BDNs and periodic stock takes of fuel tanks. While simple, Method A is prone to administrative errors and fails to capture fuel consumption during specific operations (e.g., transit vs. dynamic positioning).

- Method B (Fuel Tank Monitoring): Monitoring fuel tank readings using sounding pipes, pressure transmitters, or radar gauges. This requires temperature corrections to account for density changes in warm vs. cold climates, as diesel density varies by approximately 0.0007 kg/L per degree Celsius.

- Method C (Flow Meters): Direct measurement of fuel flow to engines and boilers using Coriolis flow meters. Coriolis meters measure mass flow directly rather than volume, eliminating the need for temperature density corrections and providing the highest level of accuracy (often within 0.1%).

- Method D (Direct Emissions Measurements): Direct measurement of CO2 concentrations in the exhaust stack using gas analyzers. This requires specialized continuous emissions monitoring systems (CEMS) which are expensive to install and maintain.

Implementing these methods requires digital planned maintenance systems, flow meters, and verified carbon accounting. Failing to comply can lead to significant penalties, port detentions, and damage to charterer relationships. Furthermore, this data collection serves as a direct precursor to including smaller vessels in the ETS in the future.

The Dutch Green Deal: Driving Local and Inland Decarbonisation

In addition to EU-wide regulations, local initiatives are accelerating the transition. In the Netherlands, the *Green Deal Zeevaart, Binnenvaart en Havens* (Green Deal Maritime, Inland Shipping and Ports) sets ambitious local targets.

Inland Shipping Targets

The Netherlands is home to Europe's largest inland fleet, operating along the Rhine and Maas rivers. The Green Deal targets:

- By 2030: A 40% to 50% reduction in CO2 emissions compared to 2015, and at least 150 inland vessels operating with zero-emission powertrains.

- By 2050: A virtually zero-emission and climate-neutral inland shipping fleet.

- Zero Emission Services (ZES): A major Dutch initiative utilizing swappable battery containers ("ZESpacks") containing up to 2 MWh of lithium-iron-phosphate (LFP) cells. These containers allow inland vessels to exchange depleted battery packs at port stations in under 15 minutes, eliminating charging downtime. The ZES infrastructure uses standardized connections and operates on a pay-per-use electricity model, lowering the upfront capital barrier for operators.

- Hydrogen Integration: The Dutch inland fleet is also pioneering hydrogen fuel cells, as seen on the vessel *Antonie*, which utilizes compressed green hydrogen to generate electricity for its propulsion motors. The vessel features storage tanks holding compressed gaseous hydrogen at 350 bar, providing sufficient range for long inland transits without refueling.

Maritime Shipping Targets

For sea-going vessels, the Dutch Green Deal aims for at least one zero-emission seagoing vessel in service by 2030, and a 70% reduction in CO2 emissions by 2050 compared to 2008.

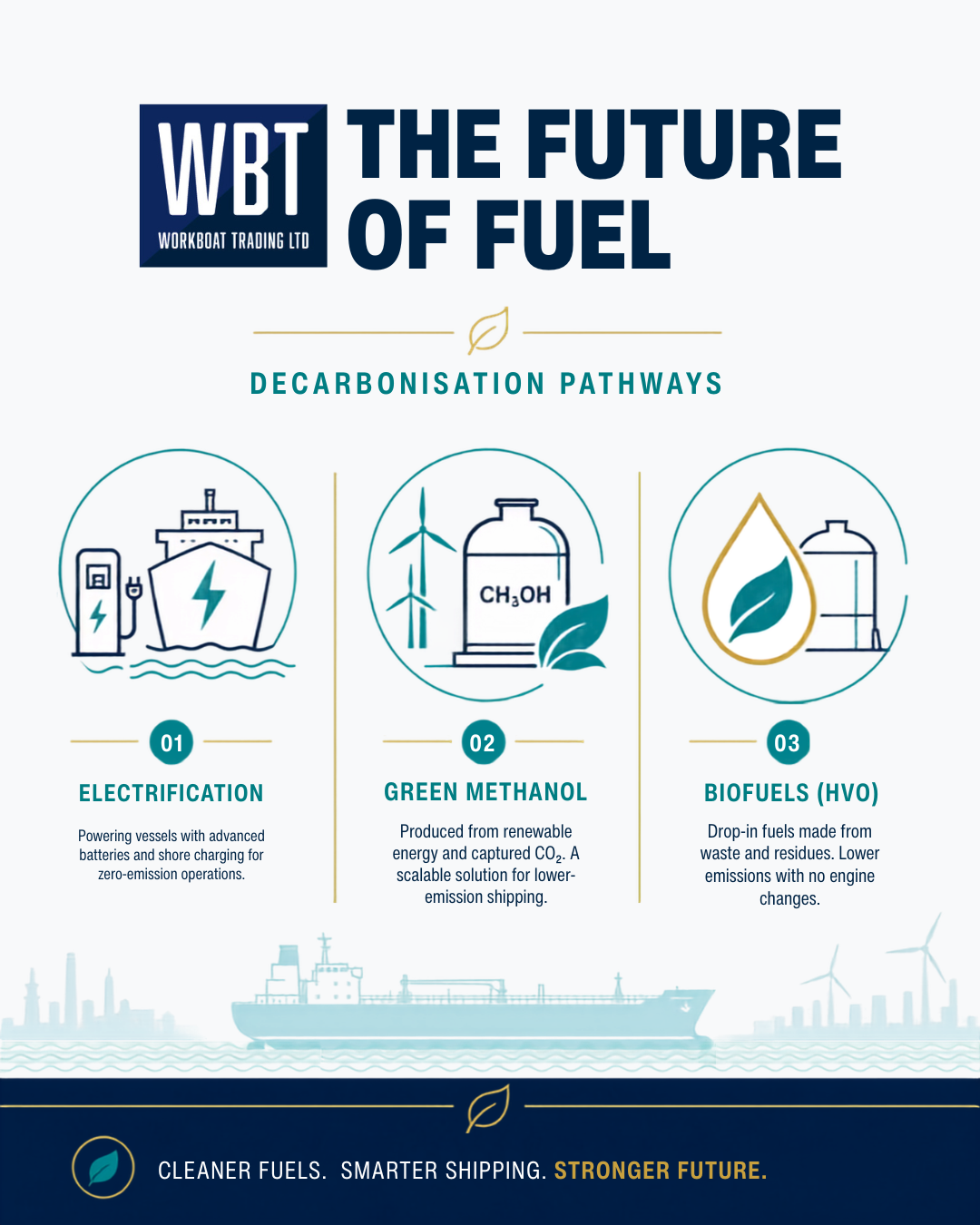

Decarbonisation Pathways: Electrification, Methanol, and Biofuels

Workboat operators are deploying several technical solutions to meet these targets:

Electrification

Highly suited for short-range harbor craft, passenger ferries, and wind farm CTVs that operate on fixed routes. Battery-electric propulsion provides zero tailpipe emissions and high efficiency. LFP batteries are favored for marine applications due to their thermal stability and long cycle life. LFP has a typical energy density of 140–160 Wh/kg, which requires careful weight distribution and structural reinforcement during vessel design.

Alternative Fuels: Methanol

Larger offshore vessels are transitioning toward methanol-ready propulsion systems. Methanol provides high energy density compared to batteries and can utilize existing bunkering infrastructure with minor modifications. Using green methanol (produced from renewable hydrogen and biogenic carbon) reduces greenhouse gas emissions by up to 95%. Methanol has approximately half the volumetric energy density of diesel (15.6 MJ/L vs 36 MJ/L), meaning vessels require twice the storage volume to maintain the same range, which impacts cargo holding and deck space.

Drop-in Biofuels

For existing fleets, Hydrotreated Vegetable Oil (HVO) and B100 biofuels represent immediate solutions. HVO (a paraffinic renewable diesel) can be used as a 100% drop-in fuel in conventional diesel engines, reducing carbon intensity by 85–90% without requiring expensive engine modifications. HVO features a low cloud point (down to -20°C), making it highly reliable in cold Northern European winters compared to standard Fatty Acid Methyl Ester (FAME) biofuels, which are prone to fuel gelling, microbial growth, and filter clogging in cold conditions.

Pan-European Regulatory Synergy: ECAs, UK Policies, and EU Alignment

Operators working throughout northern Europe must navigate a highly integrated web of national and international environmental zones.

Emission Control Areas (ECAs)

The North Sea and Baltic Sea are designated as Emission Control Areas (ECAs) under the IMO's MARPOL Annex VI.

- SECA (Sulphur Emission Control Area): Limits the sulphur content of fuel oil to 0.10% m/m, forcing operators to use marine gas oil (MGO) or alternative fuels. This restriction eliminates the use of heavy fuel oil (HFO) unless the vessel is fitted with an exhaust gas cleaning system (scrubber).

- NECA (Nitrogen Emission Control Area): Requires all vessels built after 1 January 2021 to meet Tier III NOx standards when operating in the North Sea and Baltic Sea. Tier III requires a 74% reduction in NOx emissions compared to Tier II, typically achieved through Selective Catalytic Reduction (SCR) systems using urea (AdBlue) injection or clean gas fuels.

UK Clean Maritime Plan and ETS

Following Brexit, the UK has implemented its own Clean Maritime Plan alongside the UK Emissions Trading Scheme (UK ETS).

- UK ETS Target: The UK ETS operates similarly to the EU ETS, capping emissions and requiring allowance purchases. The UK government is actively reviewing the inclusion of domestic maritime transport in the UK ETS, aiming to align its scope with the EU framework to avoid carbon leakage. This would ensure that voyages between the UK and continental Europe face comparable carbon costs.

- Clean Maritime Plan: Recommends that all new vessels for domestic routes should be designed with zero-emission propulsion capabilities from 2025.

This alignment across Northern Europe means that compliance with EU regulations ensures seamless operability. A vessel equipped with Tier III engines and a green monitoring system under the EU MRV is well-positioned for immediate deployment in UK, German, or Norwegian waters. Dual-compliant vessel certifications are highly valuable, reducing administrative hurdles when moving tonnage across the English Channel or into Scandinavian waters.

For operators looking to acquire green assets or list compliant tonnage, check the vessel marketplace, register a vessel at sell listings, or read technical updates on classification surveys and hull material selection for structural performance metrics.

Conclusion

Environmental compliance is no longer just a regulatory cost; it is a major factor in asset depreciation, charter eligibility, and resale value. As EU MRV rules expand and the EU ETS begins to cover offshore vessels, fleet operators must adapt. By investing in clean propulsion and maintaining accurate emissions profiles, operators can protect their fleet value, win premium charters, and leverage cross-border opportunities in an increasingly carbon-conscious European market.

FAQ

Does the EU ETS apply to small crew transfer vessels (CTVs) under 5,000 GT?

No, the EU ETS currently only applies to commercial vessels above 5,000 GT. Offshore support vessels above 5,000 GT will enter the scheme in 2027. Smaller vessels under 5,000 GT are currently exempt from purchasing allowances but are under active regulatory review.

What are the immediate MRV requirements for offshore support vessels starting in 2025?

Since 1 January 2025, OSVs and general cargo ships between 400 and 5,000 GT must monitor and report their carbon emissions, fuel consumption, and operational activity to the EU database. This requires establishing verified data collection plans.

How does FuelEU Maritime calculate GHG emissions?

FuelEU Maritime calculates greenhouse gas intensity on a "well-to-wake" basis. This accounts for the entire fuel lifecycle—from extraction and production (well-to-tank) to combustion on board the vessel (tank-to-wake)—encouraging the adoption of sustainable fuels.

How do Dutch Green Deal targets compare to UK Clean Maritime targets?

Both frameworks aim for rapid decarbonisation. The Dutch Green Deal targets a 40–50% reduction in inland shipping CO2 emissions by 2030 and 150 zero-emission vessels. The UK Clean Maritime Plan recommends that all new vessels ordered for domestic routes from 2025 be equipped with zero-emission propulsion.

Can green workboats command a resale premium on platforms like WBT Singapore?

Yes. As carbon compliance mandates take effect across Europe, demand for electric, hybrid, and biofuel-ready vessels is increasing. Compliant vessels maintain their asset value better and sell faster than older, diesel-only assets. Review our how-it-works page to learn how WBT supports high-value vessel transactions.